My HELOC

You have a home equity line of credit—now what?

Thanks for Choosing Sandia Area for your Home Equity Line of Credit!

Your HELOC is a flexible tool that can help you tackle big projects, manage expenses, or prepare for the unexpected. On this page, we’ll walk you through how it works—heres what you can expect during each phase of your HELOC—and how to make the most of your funds.

The Two Phases of Your HELOC

Your HELOC is divided into two key phases: the draw period and the repayment period.

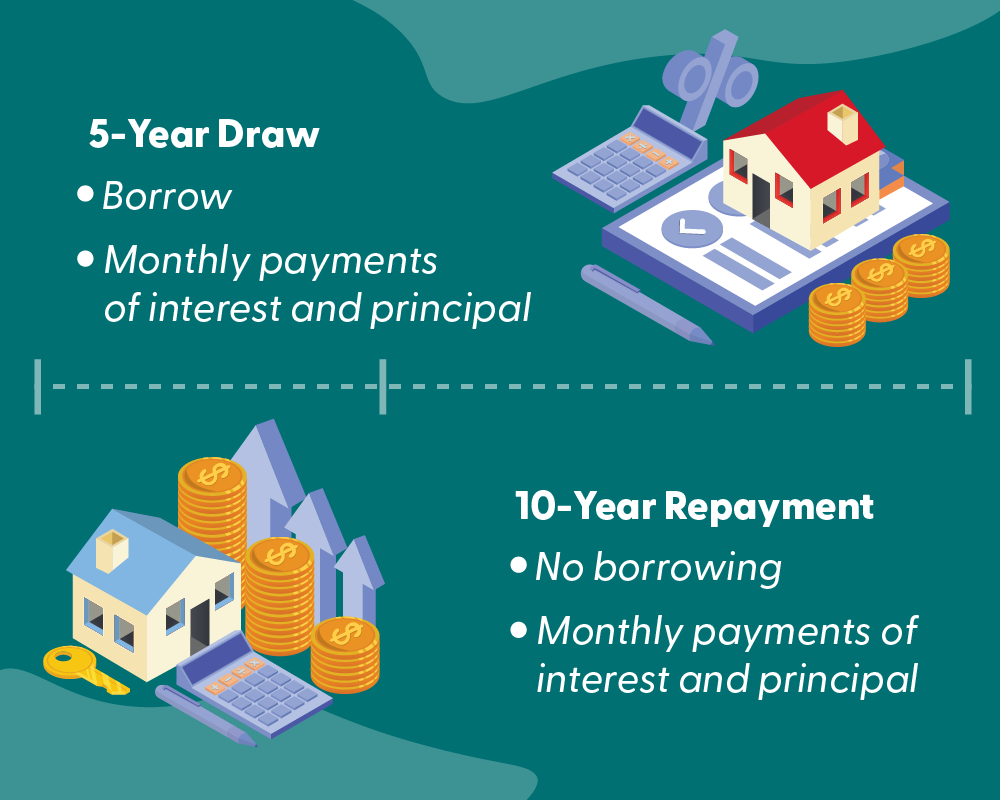

The first five years of your HELOC is known as the draw period.

- This is when you: borrow!

- Payments: Interest acrrues on only the borrowed funds. Monthly payments include that interest and a portion of the principal.

- Ready to make a draw? Each withdrawal must be at least $250.

The next 10 years of your HELOC, you’ll enter repayment.

- This is when you: repay! You can no longer borrow funds during this period.

- Payments: Your monthly payments will consist of both principal and interest as you steadily pay down your balance.

How to Use Your HELOC in 3 Simple Steps

![]()

Decide how much you need

During your 5-year draw period, you can borrow from your available credit line as needed—whether it’s for a renovation, major purchase, or unexpected cost. Think about how much you need now, knowing you can draw more later if needed.

![]()

Transfer funds to your preferred account

Transfer money from your HELOC account into another account such as a Sandia Area checking or savings account, and then withdraw or use the funds from that account. Log into your online banking or give us a call to complete a transfer.

![]()

Use your funds, then repay over time

Once the money is in your account, you’re ready to use it. During the 5-year draw period, you’ll make monthly payments based on the amount you’ve borrowed. Your rate is variable—so if the Prime Rate goes down, your rate may too. After the draw period ends, you’ll enter a 10-year repayment period, where payments will include both principal and interest but no additional draws can be made.

Federally insured by the NCUA. An Equal Opportunity Lender. Home Equity Line of Credit is a revolving credit line and is a variable APR (Annual Percentage Rate) based on the value of an index plus a margin and is subject to increase. The index is the NY Prime Rate published in the Money Rates column of the Wall Street Journal and is 7.50% as of 12/20/2024. When a range of rates has been published, the highest rate will be used. The current margin could range between 0.50% - 1.50% and is subject to change based on your credit score. The HELOC has a floor of 3.75% and a ceiling of 18.00% and will change by no more than 0.25% per month. Restrictions Apply. See your HELOC terms for details.

1. Debt Protection: Your purchase of Debt Protection with Life Plus is optional and will not affect your application for credit or the terms of any credit agreement required to obtain a loan. Certain eligibility requirements, conditions and exclusions may apply. Please contact your loan representative or refer to the Member Agreement for a full explanation of the terms of Debt Protection with Life Plus. You may cancel the protection at any time. If you cancel protection within 30 days, you will receive a full refund of any fee paid. A manufactured home cannot be used as collateral for a home equity loan or line of credit.

Go to main navigation